- China’s Dominance in the Global Luxury Market

China holds a commanding 22% share of the global luxury goods market, making it a critical player in luxury consumption worldwide. Leather goods top the list, accounting for 23.5% of the market share. Limited raw materials and production constraints have created high barriers for entry, resulting in a strong concentration of top-tier brands like Louis Vuitton and Gucci. In fact, purchasing luxury bags in France, the fashion capital, remains the most cost-effective. A price comparison between official websites for popular LV and Gucci handbags shows that prices in mainland China are 30-40% higher than the most affordable options in France.

数据来源:品牌官网 (注:价格统一按2022-12-30汇率换算成人民币统计)

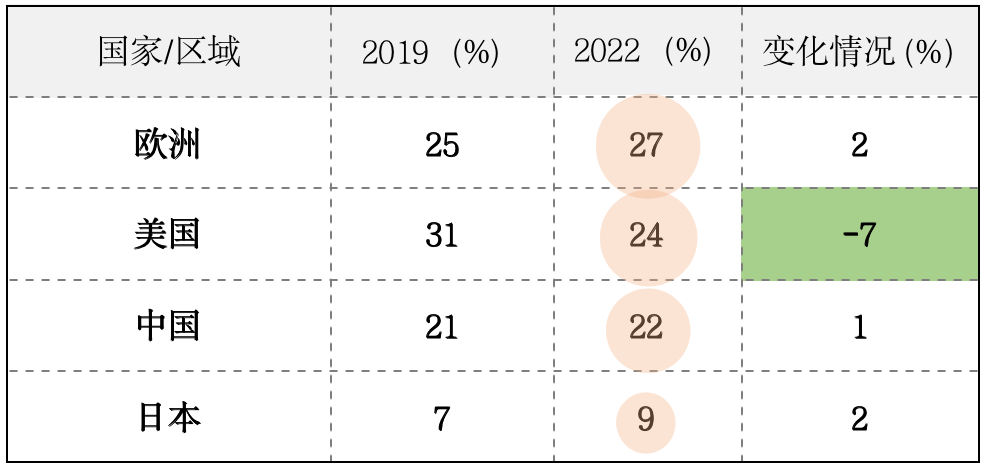

Despite the steep prices, Chinese consumers show no signs of being deterred from buying luxury items. In 2022, China’s share of the global luxury goods market reached 22%, nearly matching the United States’ 24%. Yet, the number of high-net-worth individuals in China, typically defined as those with investable assets over $1 million, is only a quarter of the US’s. This disparity raises the question: why are Chinese consumers so drawn to luxury goods, and who exactly is purchasing them in China? The fervor for luxury items persists, with consumers braving long waits and empty stock shelves, all in the pursuit of high-end products.

2022年奢侈品市场份额

数据来源:PwC analysis, Forbes

- High Net Worth Individuals are the Core Drivers of Luxury Goods Consumption

A video from a conference held by LVMH’s Greater China regional management team recently surfaced on social media, shedding light on the brand’s customer segmentation. During the meeting, LVMH classified their clients into three categories. The first two groups are ultra-high net worth individuals, those with annual personal incomes of over 10 million yuan and those earning between 3 million and 10 million yuan. Interestingly, LVMH considered individuals with incomes under 3 million yuan as falling into the “no income” category. The classification highlights a distinct divide, where even a senior executive earning 1 million yuan annually is considered on the same level as a staff member with a salary of 100,000 yuan, as long as they walk into an LV store. While this perspective may bring some humor, it also offers a glimpse into the mindset behind luxury brand targeting and consumer anxiety over income inequality.

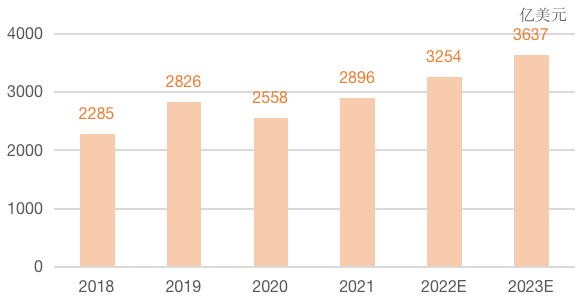

LVMH’s customer segmentation isn’t without justification. The global luxury goods market reached nearly $290 billion in 2021, marking a 13.2% year-on-year increase, and rapidly rebounding past pre-pandemic levels despite the global COVID-19 crisis. The primary driver of this growth is the expanding purchasing power of high-net-worth individuals.

全球奢侈品市场规模

数据来源:PwC analysis

According to Euromonitor, in 2020, personal luxury goods consumption from high-net-worth individuals (defined as those spending more than 5,000 euros annually) amounted to 226 billion euros. Though the total figure represented a 23.1% decline from the previous year, the share of luxury consumption from high-net-worth individuals grew by 8.4%, driven largely by a 16.7% increase in spending by those who exceed 20,000 euros annually. This reflects a broader trend: even during times of reduced spending, the wealthiest consumers continue their high-end purchases, fueling the luxury market’s growth.

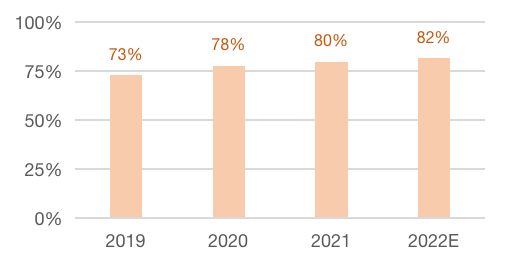

In China, high net worth individuals accounted for 80% of the luxury consumption in 2021, and this share is increasing every year. The distinction between individuals earning 3 million yuan and 30,000 yuan annually may seem less significant when looking at luxury brand clientele. While long queues at luxury stores are common for regular shoppers, the true VIPs are often whisked away to private areas or have their purchases delivered directly to their doors.

数据来源:2022中国高净值消费者洞察报告

- Luxury Brands “Harvesting” from Lower-Tier Cities: A Surge in Purchasing Power

Recent news of Louis Vuitton’s upcoming price hike, scheduled for February 18, has intensified the fervor in China’s luxury goods market. With price increases ranging from 8% to 20%, many consumers are being bombarded with messages that suggest purchasing now will save them money in the long run. Prominent phrases like “luxury goods are an investment and an asset for preservation” and “buy now or miss out on a 20% discount” have penetrated consumer consciousness, fueling a sense of urgency.

Industry experts point to two main reasons for these price hikes: first, the need to adjust prices in response to rising production costs and global inflation; and second, the pandemic’s impact, which has limited international travel, shifting high-end consumption to domestic markets. Although the idea of “buying now before prices go up” contradicts conventional consumption habits, it taps into consumers’ desire for the “scarcity” and “uniqueness” that luxury goods embody.

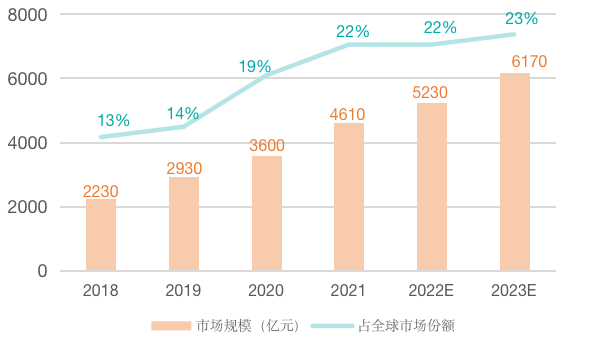

中国奢侈品市场规模及市场份额情况

数据来源:PwC analysis

Furthermore, the price increases have reinforced the idea of luxury items as investments, drawing in a new customer base. Many consumers who previously viewed luxury goods as ordinary consumer products are now beginning to see them as valuable assets. This shift indicates a notable trend toward “market sinking,” as data reveals a steady increase in luxury goods penetration in third-tier cities and below. From 2019 to 2021, market penetration in these cities grew from 38% to 46%, nearly on par with first and second-tier cities.

While luxury brands may not consider the “no income group” as their primary target, they are still keen to tap into this expanding market. In January 2023, the Louis Vuitton store in Hefei Yintai Centre set a record for monthly sales, exceeding one billion yuan. Long queues in second and third-tier city stores reflect the growing number of new customers in these markets and highlight their immense potential. For instance, while Shanghai’s Hang Lung Plaza saw a 10% decline in revenue, Hang Lung Plazas in cities such as Dalian, Wuhan, Wuxi, and Kunming reported revenue growth ranging from 6% to 52%. This shift underscores the growing purchasing power of affluent customers outside of luxury brands’ traditional core markets.

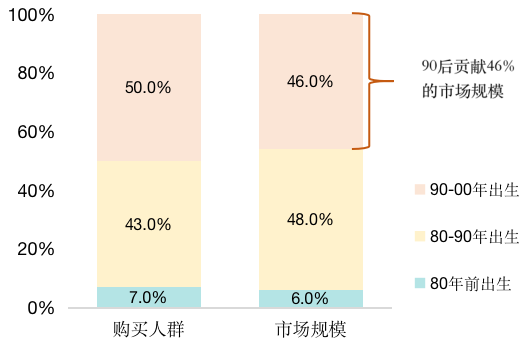

- Youth as the Driving Force of Luxury Goods Consumption: The New Faces of Affluence

In 2021, the post-90s generation accounted for 50% of luxury goods consumers in China, solidifying their position as the dominant group in the country’s luxury market.

2021年我国奢侈品消费主力人群

数据来源: BCG, 申万宏源

The growing popularity of luxury items among young people can be attributed to two primary factors: first, their strong purchasing power. Many post-90s individuals are not burdened by financial commitments like home ownership, car payments, or raising children, which leaves them with more disposable income. Second, their consumption is heavily influenced by “circle culture,” where purchasing certain luxury goods often represents a shift in identity or mindset.

Luxury brand Balenciaga, for example, blends street culture, rebellion, and art into its brand image. For young people, acquiring items like Balenciaga’s dad shoes or motorcycle bags can symbolize breaking free from traditional expectations. Similarly, as they enter the workforce, items like Louis Vuitton’s Neverfull and Onthego bags serve as markers of adulthood and social mobility, signaling the shift from student to professional identity. According to the Bain Luxury Goods Study, it is projected that by 2025, millennials and those under 25 will dominate the luxury goods market, making up 65-70% of the total consumer base.

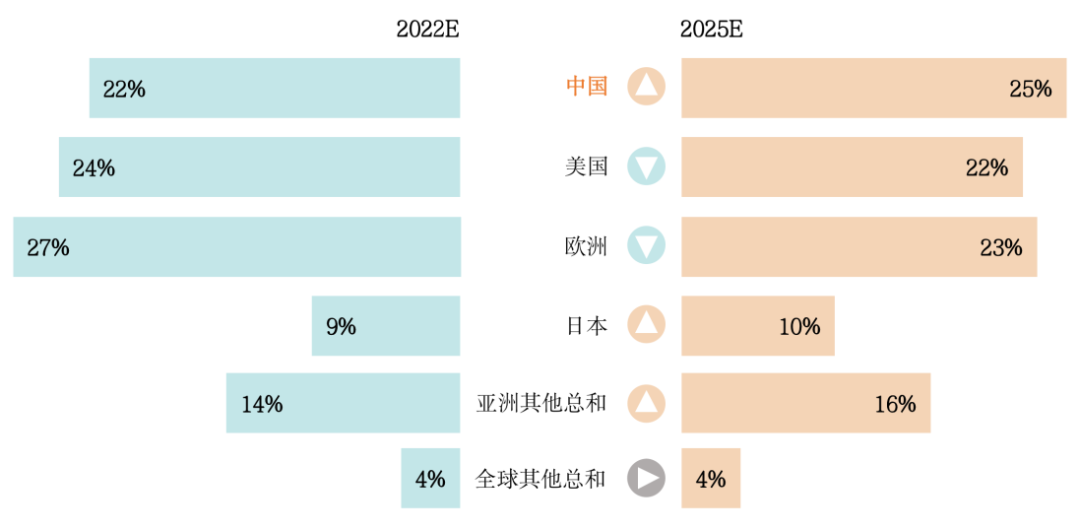

- China’s Path to Becoming the World’s Largest Luxury Market

China’s luxury market is fueled by a stable base of high-net-worth individuals, a burgeoning customer base in second and third-tier cities, and a young consumer demographic that is fast becoming the primary driver of demand. PwC forecasts that by 2025, China’s luxury goods consumption market will surpass RMB 800 billion, positioning China as the world’s largest luxury goods consumer market, accounting for 25% of the global share.

不同国家/区域奢侈品消费市场份额变化

数据来源: PwC analysis

With such a promising and expansive market, luxury brand executives are taking notice. In early February, François-Henri Pinault, Chairman and CEO of Kering (Gucci’s parent company), visited luxury consumption hubs in Chengdu, Nanjing, Shanghai, and Beijing. Johann Rupert, CEO of Richemont (the parent company of Cartier), is also expected to visit China soon, while Bernard Arnault, Chairman and CEO of LVMH, has plans for his own trip. Following these high-profile visits, Kering’s stock price rose by €27.8, or 4.95%, reflecting the optimism surrounding China’s luxury market.

The rush of luxury executives to China signals the immense opportunity they see in the country, and the “golden wheat field” they’re eager to harvest.