Despite China’s reopening, overseas sports brands face significant challenges in navigating the market. Supply chain disruptions have led to inventory issues, while a full rebound in consumer confidence remains elusive.

Established legacy brands are hitting growth plateaus, domestic competitors are rapidly advancing, and a new wave of overseas niche and influencer-driven brands is entering the still-evolving Chinese sportswear market, intensifying competition.

Community Engagement Becomes Essential for Overseas Sports Brands in China

Far from losing momentum during the pandemic, community-driven activities have become a vital tool for brands to connect with their audience. Regularly hosting community events is now a standard of active sports brands operating in China.

Initiatives like Adidas’ “On the Run” running events, Nike’s “Run 100 Lanes,” and GymShark’s “66-Day Challenge” are transforming individual sports such as running, cycling, and fitness into collective, social experiences. Meanwhile, niche markets are being cultivated through Lululemon’s Sweat Society, Nobull’s CrossFit community, and Dyson’s Ironman network, showcasing a growing emphasis on specialized sports communities.

Overseas Sports Brands Accelerate Expansion in China, Positioning as Alternatives to Giants like Nike and Adidas

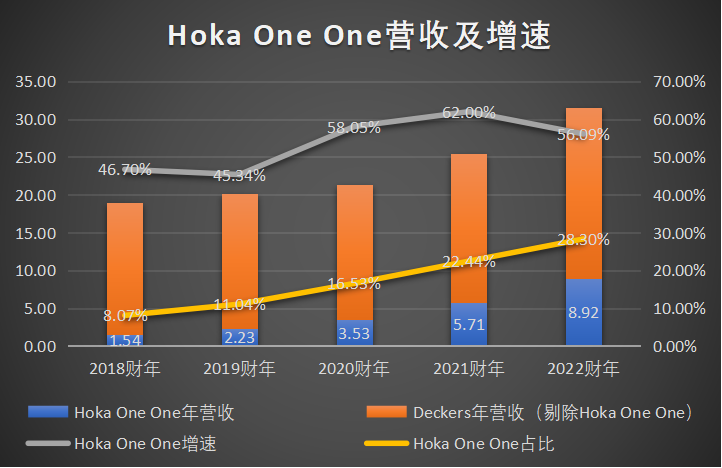

As established sports brands face growth plateaus, emerging players are seizing opportunities for counter-trend growth in the Chinese market. For instance, Hoka One One has achieved remarkable success, surpassing UGG in revenue during Q1 of the 2022 fiscal year and becoming the fastest-growing brand under the Deckers Group post-pandemic.

Other brands are also making strides. GymShark has launched a Little Red Book account and a Hong Kong office to gear up for expansion in Greater China. Vuori, a men’s yoga apparel brand reminiscent of lululemon, debuted its Tmall flagship store ahead of Double 11. Meanwhile, Silicon Valley footwear brands like On and Allbirds are rolling out store networks across Chinese cities, and Brooks has entered the market through e-commerce platforms like Tmall and JD.com.

Beyond initial market entry, many brands are deepening their presence. Lululemon continues to expand its footprint into second-tier cities, with plans to target lower-tier regions. Patagonia has followed suit, extending its reach to Guiyang, a growing second-tier city.

The segmented sportswear market in China remains a “blue ocean” for domestic and international brands, offering substantial opportunities for niche players. However, competition with affordable alternatives poses challenges. For instance, while lululemon yoga pants are celebrated for their quality, many consumers opt for budget-friendly options that offer similar elasticity and comfort without the concerns of maintenance or durability.

As a result, the next wave of overseas brands entering China is poised to position itself as cost-effective alternatives to established giants like Nike, Under Armour, and lululemon, catering to a price-sensitive yet quality-conscious consumer base.

Balancing Quality and Affordability

While international brands once held strong appeal in China, local consumers have developed a sharper cultural awareness and are no longer swayed solely by foreign labels.

Issues like inconsistent quality control and high price points have dampened enthusiasm for some brands. Even loyal Lululemon customers are beginning to reconsider, while Vuori’s recent entry into the Chinese market has already faced backlash over pricing.

Chinese consumers are willing to invest in high-quality, professional products but are increasingly discerning, resisting blind spending on premium offerings.

The growing presence of niche brands highlights the vast untapped potential of China’s sportswear market. The clothing penetration rate in China still lags significantly behind that of developed markets like the United States, where average annual spending on sportswear exceeds $300, nearly ten times the current level in China.

This gap, combined with rising demand for specialized apparel, positions overseas professional brands as formidable competitors in China’s evolving sportswear landscape.

Focusing on Functionality and Trendiness

Post-pandemic, the rise of mountain casual fashion and outdoor sports has significantly influenced consumer preferences.

One overlooked opportunity is the demand for premium yet stylish functional products among middle-class men. Patagonia’s success stems from its ability to blend luxury positioning with strong functionality and appealing aesthetics, addressing the needs of this demographic.

For urban professionals, outdoor activities symbolize a form of luxury. The choice of outdoor brand reflects their identity, projecting labels like “middle-class,” “elite,” and “healthy lifestyle.”

Patagonia’s popularity is just the beginning, as more brands are pivoting toward men’s apparel, aligning with the growing “him economy.” Lululemon has identified its men’s product line as a pivotal growth driver, while Vuori has strategically targeted this market with its sports and leisurewear.

Middle-class men increasingly seek products that combine functionality, aesthetic appeal, and social symbolism. Brands that deliver these elements can establish strong resonance with this consumer base.

The Decline of Luxury in Sportswear Consumption

In the post-pandemic era, marked by economic uncertainty and tightened consumer budgets, the trend of “consumption downgrading” has reshaped spending habits. High-end fitness products, once a symbol of aspirational living, are now facing reduced demand as consumers prioritize affordability.

Premium fitness consumables, carrying significant price premiums, have become targets for budget-conscious shoppers. Even established brands like Lululemon have had to adjust to these market shifts by increasing discounts.

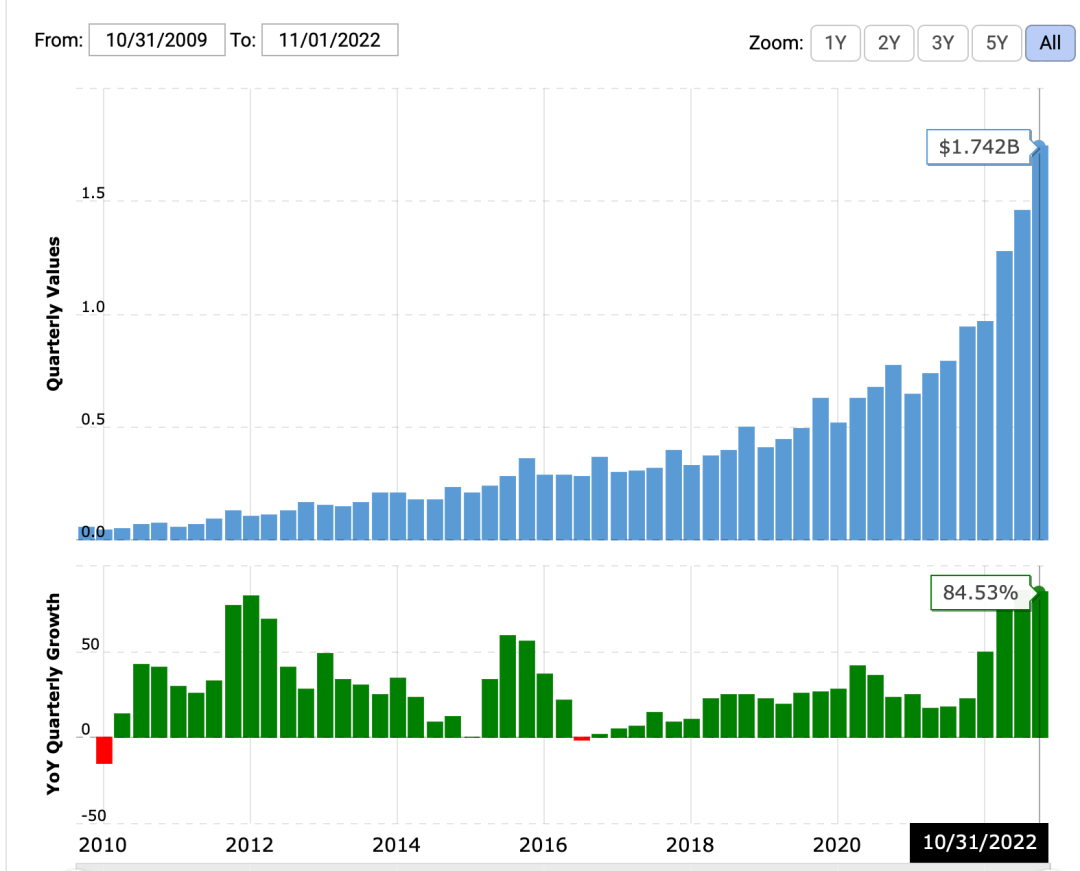

According to analyst reports, Lululemon’s average discount rose by approximately 470 basis points year-over-year in November. For the 2023 Chinese New Year, the brand offered an unprecedented 7.7% discount with full reductions, alongside steep discounts like 75% off in its local Canadian market.

Lululemon’s inventory levels reached historic highs, reflecting a broader challenge shared by traditional fitness brands like Nike and Adidas. However, aggressive discounting is proving to be a double-edged sword. Many consumers report that frequent discounts devalue the brand and diminish their desire to purchase.

数据来源:lululemon2022年第三季度财报

While fitness enthusiasts are becoming more discerning, they haven’t stopped spending entirely. Instead, they are increasingly drawn to cost-effective sportswear that balances quality and price, signaling a shift in priorities within the fitness apparel market.