Clothing and transportation are essential aspects of daily life, and in post-pandemic China, these sectors are showing signs of recovery. While the real estate market struggles to regain momentum and the food industry remains subdued, the textile and clothing sector has delivered a remarkable performance in 2024, alongside the automotive industry.

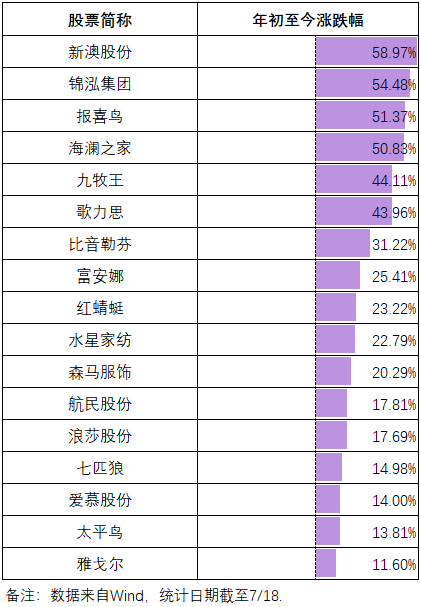

Sectors like new energy, liquor, and pharmaceuticals have shown limited improvement, but the clothing industry stands out on stock performance charts. Companies such as Jin Hong Group, Baoxiniao, and Heilan Home have experienced stock price increases exceeding 50%, signaling a noteworthy comeback for the sector.

Key Factors Driving the Rebound of China’s Clothing Industry

After years of challenges from industrial relocation to Southeast Asia and declining export orders, China’s textile and clothing sector has demonstrated resilience through self-adjustment. Here are the key factors behind its resurgence:

1. Leading Companies Expanding Against the Trend

The pandemic reshaped the domestic clothing industry’s competitive landscape, favoring leading companies over smaller players. While many small and medium-sized enterprises reduced store counts or exited the market, major publicly-listed firms expanded strategically.

In 2022, Haier Leng increased its store count by 270, Beinlefin opened 91 new outlets, Ge Lisi expanded by 63 stores, and Baoxiniao added 8 more locations. Although Jin Hong Group only opened one physical store, its online sales revenue share grew significantly, rising from 33.20% in 2021 to 38.88% in 2022.

The pandemic acted as a catalyst for the industry’s “survival of the fittest” scenario, where leading companies gained substantial market share and saw more favorable stock performance.

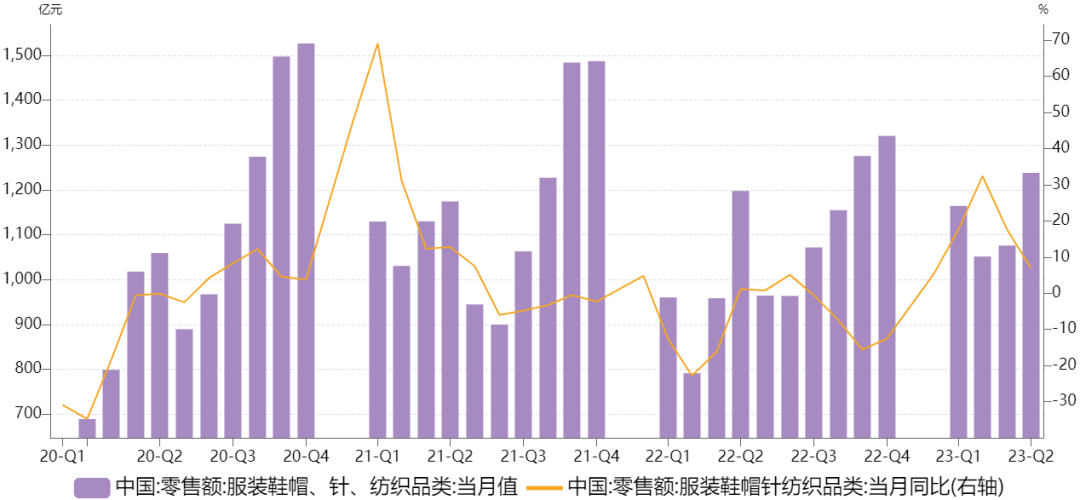

2. Significant Year-on-Year Retail Growth

Retail data indicates a marked recovery for the textile and clothing sector, with noticeable year-on-year growth in monthly retail sales during the first half of 2024. This data underscores the industry’s bounce-back, supported by improved consumer confidence and spending.

3. Increased Business Confidence

Despite the challenging market conditions in 2024, the importance of confidence has become more evident, with many now fully embracing the saying, “Confidence is more precious than gold.”

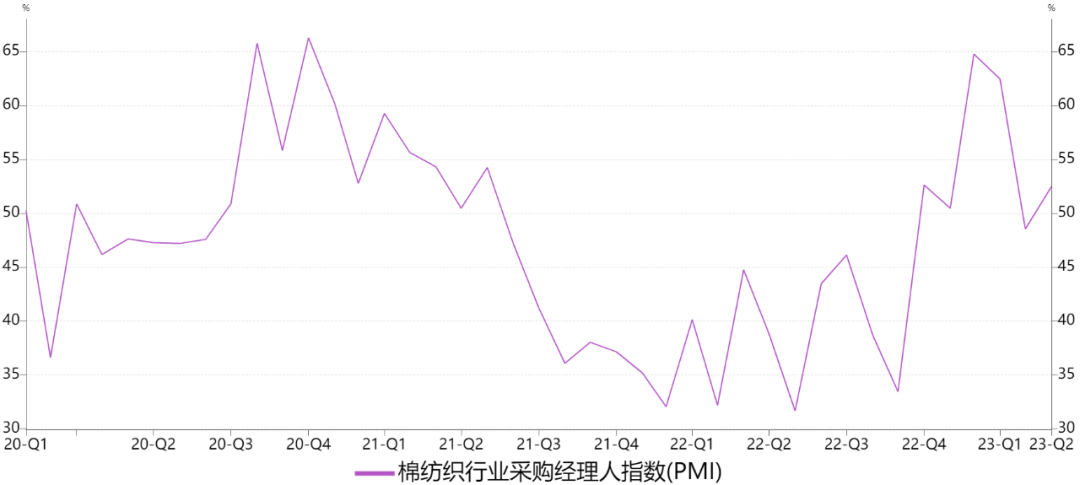

In the textile and clothing industry, the Purchasing Managers’ Index (PMI) began to rise sharply in December 2022, surpassing the 50 thresholds. By February and March 2024, it even exceeded 60. Although it briefly dipped below 50 in April, it rebounded quickly in May, signaling a renewed sense of optimism and confidence in the sector.

Emerging Trends in Chinese Fashion Consumption in 2024

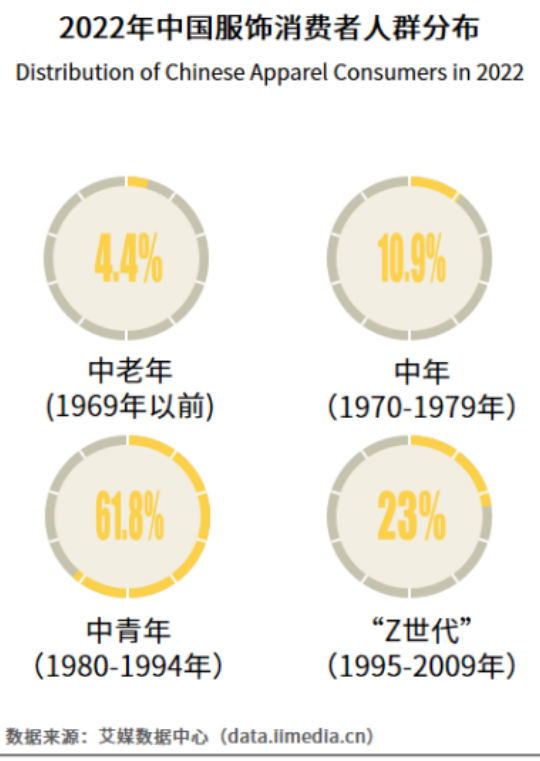

The clothing industry has experienced significant transformations in recent years, with domestic brands steadily gaining influence. The “Z generation,” particularly those born in the mid-1990s, is increasingly becoming the dominant consumer group in the fashion sector. This group tends to favor brand consumption, values their purchases more highly, and demonstrates stronger brand loyalty. As their purchasing power continues to grow, they are expected to drive further changes in the industry.

Additionally, there is a growing willingness among consumers to invest in clothing, which is a key factor in the recovery of the fashion industry.

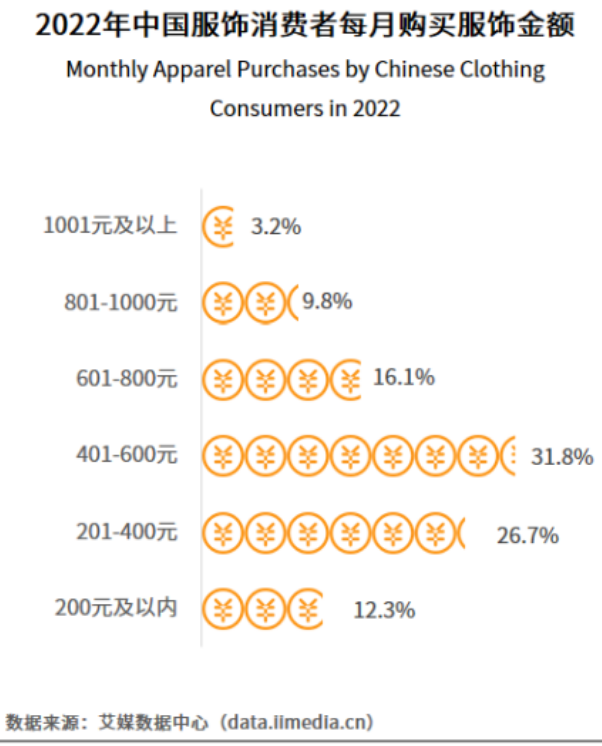

Data shows that most Chinese clothing consumers spend between 201 and 600 RMB per month on apparel. Of these, 31.8% fall within the 401-600 RMB range, while 26.7% spend between 201 and 400 RMB. The majority of consumers (62.7%) make clothing purchases 2 to 3 times a month, reflecting a steady demand in the sector.